Obama just announced that they'll allow the government agencies responsible for financing the housing bubble to try to prop that bubble up by allowing refis of up to 125% of the house's "value" (original price?). I can't imagine who'd buy such an instrument from them, but just a word to the wise, don't do it if it tempts you.

Refis are 2nd mortgages and are recourse loans; unlike 1st mortgages, if you default on a refi, they can take the house, then come after you for the rest.

Friday, June 19, 2009

Tuesday, June 16, 2009

Economics for the Citizen

Just a link post; I'd call Walter Williams my favorite economist, but I don't really have any favorites except for not-Krugman. But anyway, Walter Williams freakin' rocks, and he has small class notes for an intro econ course he teaches called Economics for the Citizen. It's both really good and also nice & short too. I highly recommend it.

Wednesday, June 03, 2009

Getting Ready for the Mortgage Defaults to Get Serious

No doom & gloom for a while, I must be losing my touch.... Here's something just to keep the stomach acids going:

There's a lot of buzz going around based on a super-big chart-filled presentation by some scare-mongers called "T2 Partners", who're attempting to use reality to scare customers into buying their services. Sadly, the reality they paint, is, well, real. Here're a few of said charts:

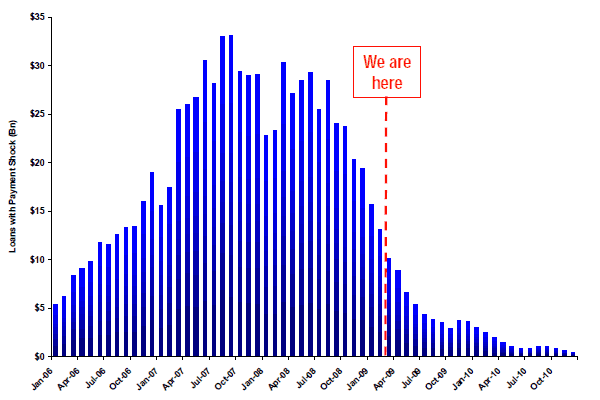

Here's the situation with regards to subprime mortgage rate resets:

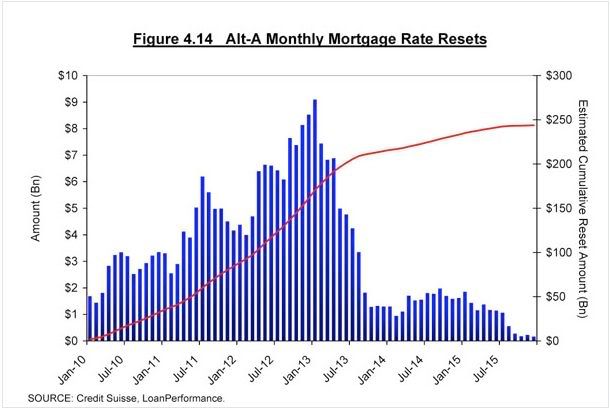

Here's where we stand with regards to the Alt-A resets...

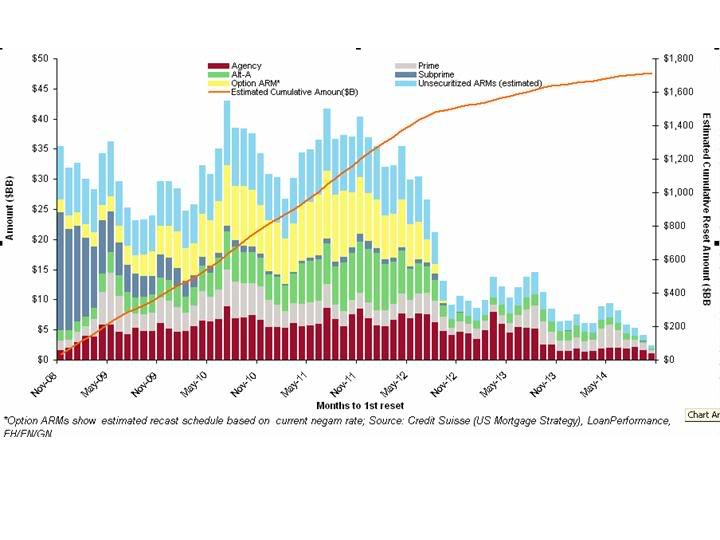

or scheduled resets in general:

The 64-thousand-dollar question of course is what this will do to bank valuations. No-one knows for sure how many of these mortgages will end up defaulting, but I'm suspecting that they're already factored into bank shares' trading prices.

With $1.7T of mortgages resetting over the next five years, during the worst economy seen in decades, the big question will be how will this affect the rest of the economy. Especially retail sales. No-one knows, but I'm wagering that those "V-shaped" recession wonks are wrong, and that the "U-shaped" wonks are also wrong. Given the way mean reversion versus a growth trend-line tends to work, I'm betting on an "L-shaped" recession that stays flat, just like the Japanese have seen (since we're repeating their mistakes).

This of course while we're debasing the currency so much that the Treasury Secretary got laughed off the stage in China.

We now return you to your regular sunshine filled day.

There's a lot of buzz going around based on a super-big chart-filled presentation by some scare-mongers called "T2 Partners", who're attempting to use reality to scare customers into buying their services. Sadly, the reality they paint, is, well, real. Here're a few of said charts:

Here's the situation with regards to subprime mortgage rate resets:

Here's where we stand with regards to the Alt-A resets...

or scheduled resets in general:

The 64-thousand-dollar question of course is what this will do to bank valuations. No-one knows for sure how many of these mortgages will end up defaulting, but I'm suspecting that they're already factored into bank shares' trading prices.

With $1.7T of mortgages resetting over the next five years, during the worst economy seen in decades, the big question will be how will this affect the rest of the economy. Especially retail sales. No-one knows, but I'm wagering that those "V-shaped" recession wonks are wrong, and that the "U-shaped" wonks are also wrong. Given the way mean reversion versus a growth trend-line tends to work, I'm betting on an "L-shaped" recession that stays flat, just like the Japanese have seen (since we're repeating their mistakes).

This of course while we're debasing the currency so much that the Treasury Secretary got laughed off the stage in China.

We now return you to your regular sunshine filled day.

Subscribe to:

Comments (Atom)